The Fading Australian Dream

You can find the latest release of this data and infographic here.

Housing affordability

Housing affordability is currently a key issue of discussion in Australia and while there are a number of factors at play, the main price driver is that demand for houses is exceeding supply. Population growth, a trend to smaller households (and so more homes needed relative to the population), and demand for homes not only from first home buyers but also from downsizers, overseas buyers, local investors, and self-managed super funds and trusts are all fuelling price rises.

While Australia’s current annual population growth of 1.4% may seem modest, this adds almost 340,000 to our population each year- which is one new Darwin every 20 weeks or a new Tasmania every 18 months.

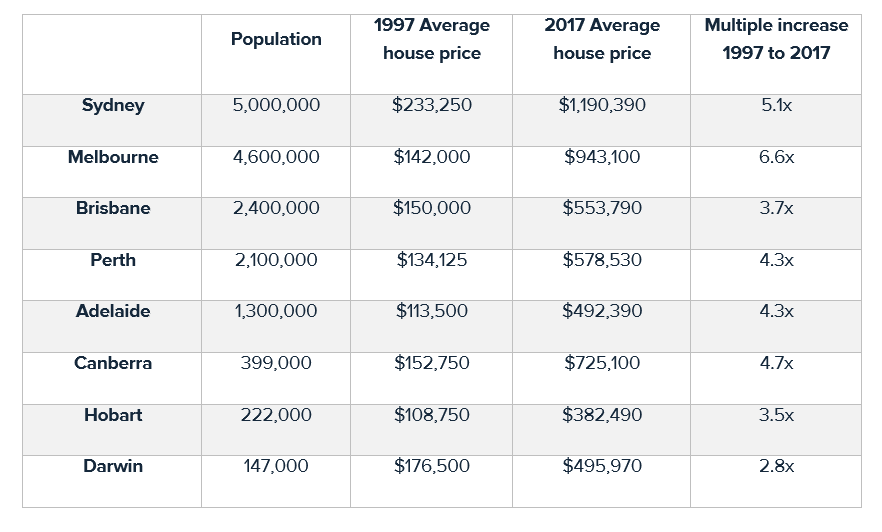

Where population growth is strongest, house price rises are the highest

Sydney is growing much faster than this having averaged 1.8% per annum for the last five years. It will add almost two million to its population by 2037 – which is the equivalent of adding a new Perth into Sydney. Melbourne is currently Australia’s fastest growing city and based on the current growth trends, it will overtake Sydney to become the nation’s largest city around the middle of this century. Unsurprisingly where population growth is strongest, house price rises are the highest.

Earnings growth has not kept up with house price growth

In just twenty years, the average Sydney house price has increased more than five-fold from $233,250 in 1997 to $1,190,390 today while in Melbourne prices over the same period have increased by more than six times from $142,000 to $943,100 today. While it is true that wages have increased over this time, earnings growth has not kept up with house price growth. In 20 years, average annual full-time earnings have not quite doubled from $42,010 in 1997 to $82,784 today.

The impact of growing demand on house prices is most evident when comparing prices to average earnings. Twenty years ago, the average Sydney house was 5.6 times average annual earnings while in Melbourne it was an affordable 3.4 times annual earnings. Today Sydney homes are more than 14 times average earnings, and in Melbourne more than 11 times annual earnings. While the maxim that house prices double every 10 years is not always the case and growth fluctuates, since 1997 Sydney prices have in effect doubled every 8 years while Melbourne has managed this every 6 years.

If the growth metrics over the last two decades play out over the next two, the average home in both Sydney and Melbourne in 2037 will exceed $6 million. Clearly, the Australian dream of home ownership for the next generation is fading. Young people today need almost three times the purchasing power that their parents needed to buy the average place, so even double incomes will not quite do it. Additionally, today’s new households are starting their earnings years later than their parents, having spent longer in tertiary studies, and they begin their economic life not with zero savings like their parents, but well into the negative- with interest accumulating study debts to pay off. Even if today’s emerging generations start saving harder and earlier and live with their parents longer, home ownership is still not a given.

Policy settings around migration and baby bonuses have grown the population and policies around property tax incentives, self-managed superannuation and investment provisions have fuelled property demand therefore policy support will be required to bring the great Australian dream a little bit closer to reality.

Sources: Population at 2017 (ABS). 1997 prices: Macquarie University (Abelson). 2017 house prices: Core Logic. Analysis: McCrindle

For media commentary contact us on 02 8824 3422 or at [email protected]