Hope on the Horizon amidst COVID-19

Hope is on the horizon as Australia moves towards its three phases of recovery. Optimism towards the future is growing with the number of Australians feeling extremely or very uncertain about the future reducing slightly since March (34% cf. 39% phase one). There is, however, still a sense of uncertainty about the future. Currently a third of Australians (34%) feel extremely or very uncertain about the future with more than half 56% feeling somewhat or slightly uncertain.

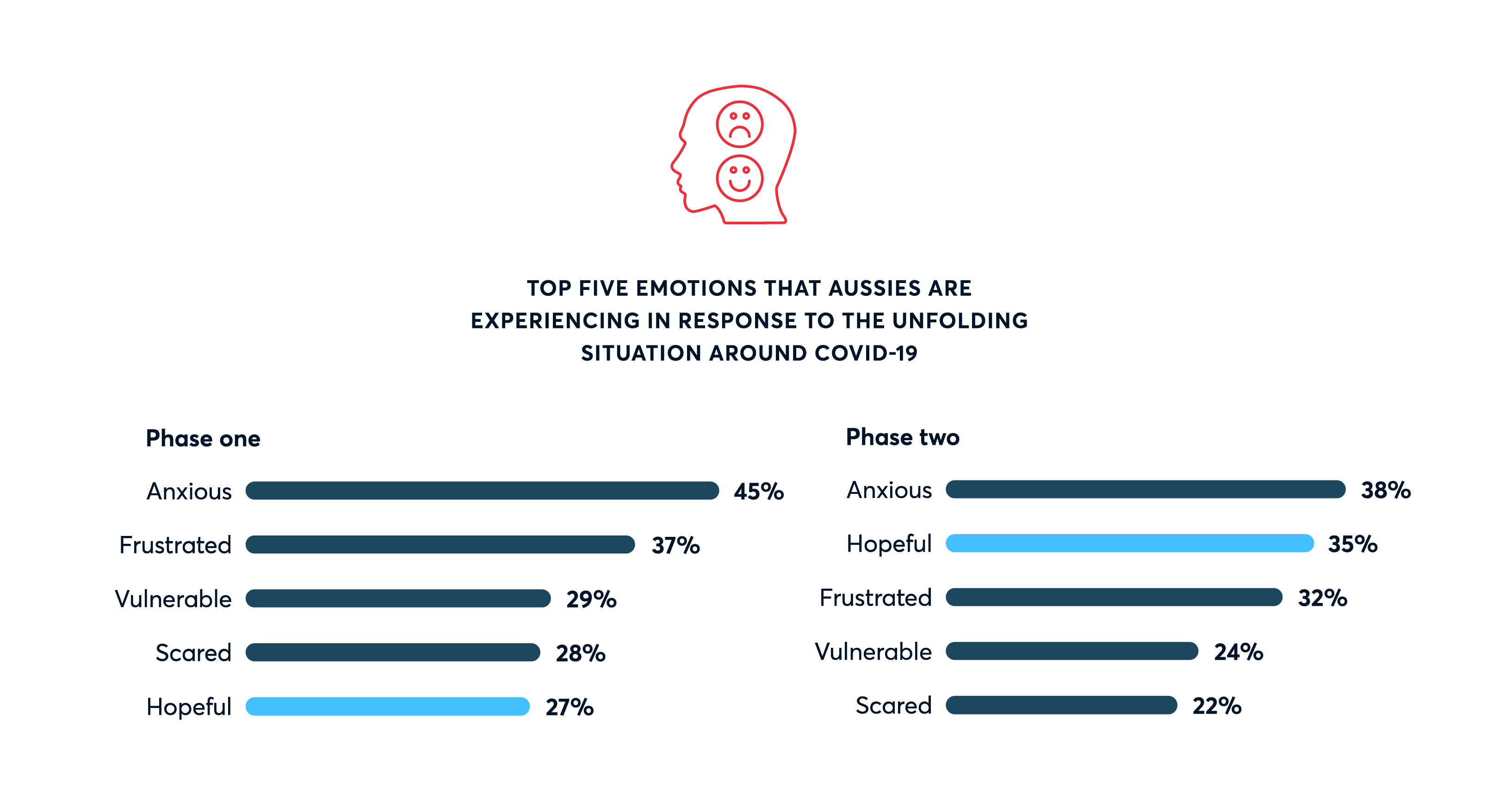

Australians are experiencing a range of emotions as they navigate the complex world of COVID-19. The most common emotion Australians are experiencing continues to be anxiety (38%), although this has reduced since March when more than two in five Australians (45%) were feeling anxious in response to the unfolding situation around COVID-19. Earlier in the year, many Australians were also feeling frustrated (37%), vulnerable (29%) and scared (28%). As Australians have adapted and the focus has shifted to the recovery, they are beginning to feel more hopeful. More than a third of Australians are now feeling a sense of hope (35%) compared to only 27% in March.

The biggest negative impact of COVID-19 has been on Australian’s social health

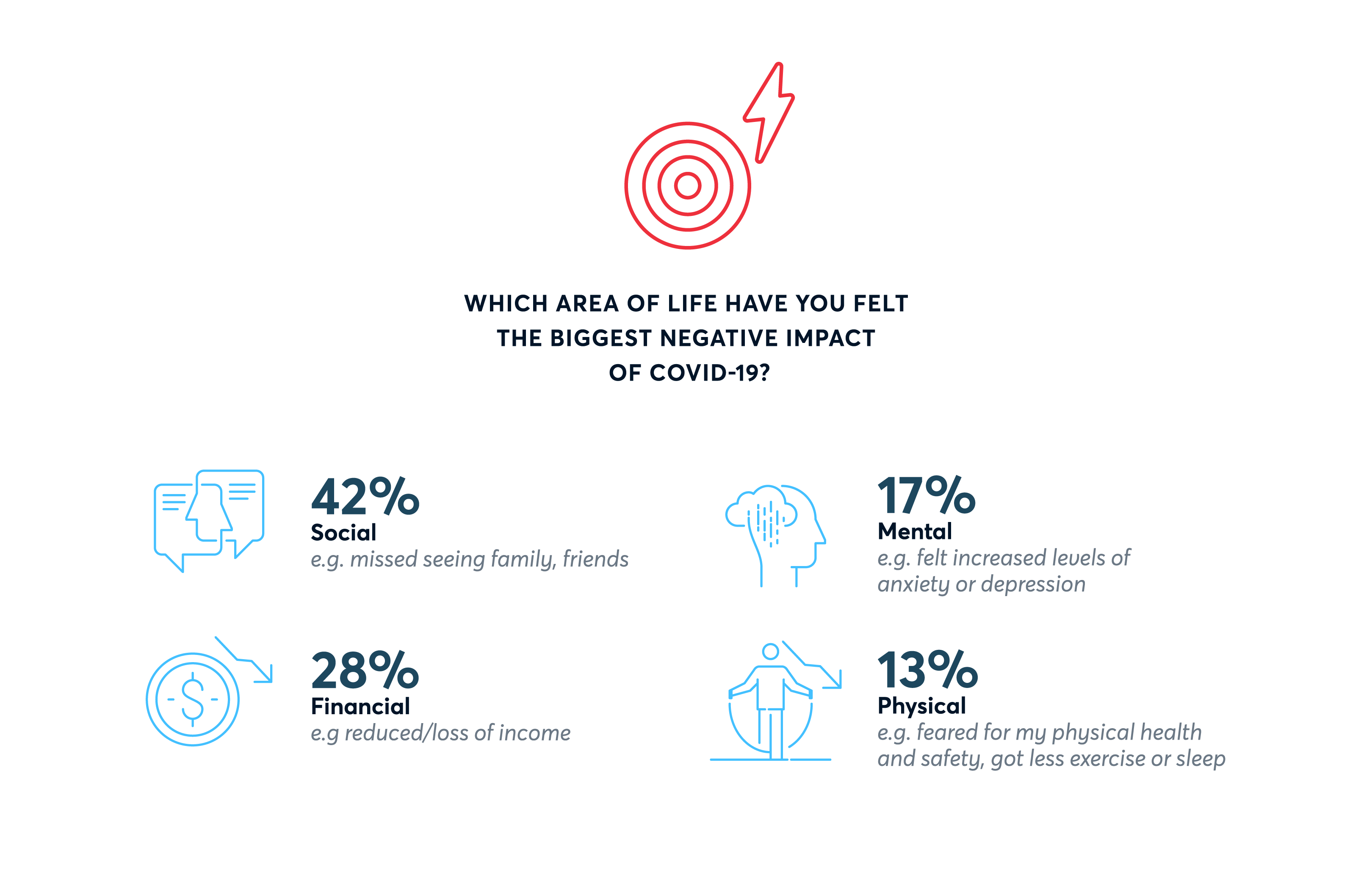

Over the last few months, Australians are most likely to have felt the biggest negative impact from COVID-19 on their social life where they have missed seeing family or friends (42%). For almost three in ten Australians (28%), however, the biggest impact has been felt financially likely through a reduction or loss of income. Many Australians have felt the negative impact from COVID-19 on their mental health (17%) with increased levels of anxiety or depression, while 13% have been most impacted physically through fearing for their physical health or getting less sleep or exercise.

Negative impacts of COVID-19 by generation

Younger generations are more likely than their older counterparts to have felt the biggest impact financially (33% Gen Z, 37% Gen Y cf. 28% Gen X, 20% Baby Boomers, 12% Builders) and mentally (25% Gen Z, 22% Gen Y cf. 17% Gen X, 11% Baby Boomers and 4% Builders).